In the rapidly evolving fintech landscape, security remains the backbone of consumer trust and operational stability. As digital transactions, mobile banking, and online lending explode in scale, cyber threats and insider risks have become more sophisticated. Traditional security measures are no longer sufficient to safeguard financial data, transactions, and digital assets. To address these challenges, cutting-edge research is exploring the integration of blockchain technology with “Zero Trust” architectures—creating a next-generation security framework for fintech platforms.

This blog explores what blockchain and Zero Trust architectures are, how they enhance fintech security, their benefits, challenges, and future adoption prospects, providing a complete overview for businesses, developers, and regulators.

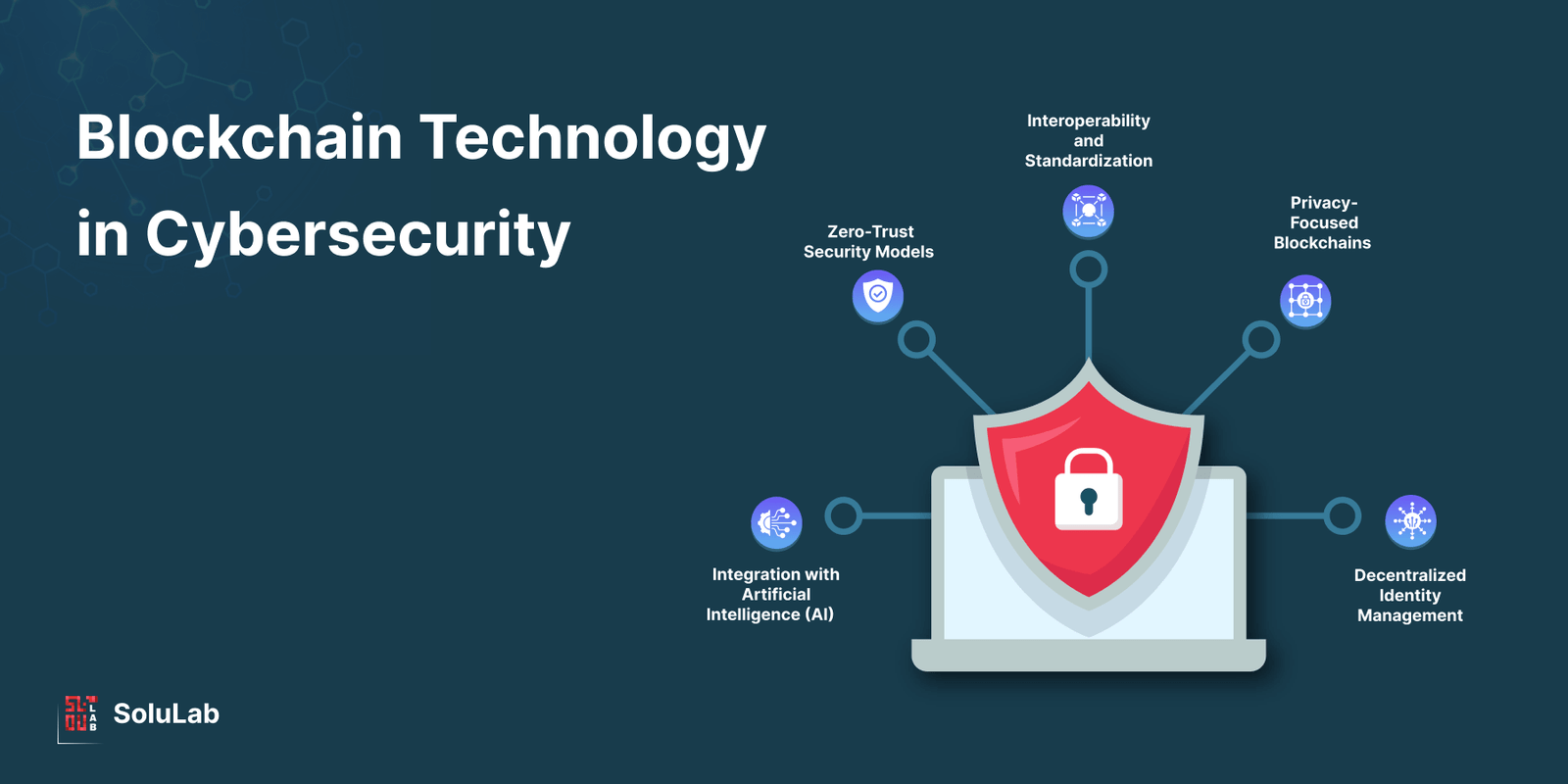

1. Understanding Blockchain in Fintech Security

Blockchain technology offers a decentralized, immutable, and transparent ledger for financial transactions. Every transaction is recorded in a block, cryptographically linked to the previous one, creating a tamper-proof chain.

For fintech, this means that sensitive financial transactions, user data, and audit logs can no longer be altered or deleted by malicious insiders or external hackers. Blockchain ensures data integrity, making fraud, double-spending, or unauthorized changes virtually impossible.

Moreover, blockchain enables smart contracts, which are self-executing programs triggered by predefined conditions. These contracts automatically enforce rules, reducing reliance on intermediaries and minimizing human error. In practice, a lending platform can automatically disburse funds only when all compliance checks pass, improving transaction accuracy and accountability.

2. Zero Trust Architecture Explained

Zero Trust is a security framework that assumes no entity—inside or outside the organization—is inherently trustworthy. Unlike traditional perimeter-based security models that rely on firewalls or network boundaries, Zero Trust enforces strict identity verification and continuous monitoring for every access request.

In fintech, Zero Trust ensures that even employees or internal systems cannot access sensitive financial data without proper authentication and authorization. Every transaction, API call, or database query is logged, verified, and continuously monitored. By combining Zero Trust with blockchain, fintech firms gain immutable audit trails and automated enforcement, creating an environment where trust is earned per action, not assumed.

3. Benefits of Combining Blockchain with Zero Trust in Fintech

The integration of blockchain and Zero Trust architecture offers several key advantages:

- Enhanced Data Integrity – Blockchain’s immutable ledger ensures that all transactions are permanent, while Zero Trust verifies the legitimacy of each action, preventing unauthorized changes.

- Reduced Insider Threats – Continuous authentication and role-based access in Zero Trust prevent employees from abusing their access privileges, while blockchain records every action transparently.

- Automated Compliance – Smart contracts and audit trails automatically enforce regulatory and internal compliance rules, minimizing human intervention and reducing errors in reporting or approvals.

- Increased Consumer Trust – Customers can verify that transactions and financial data are secure, boosting confidence in fintech platforms.

By combining these two technologies, fintech platforms can create a multi-layered security framework that addresses both external cyber threats and internal operational risks.

4. Real-World Applications in Fintech

Several fintech areas stand to benefit from blockchain + Zero Trust:

- Digital Banking – Ensuring all banking transactions, account updates, and fund transfers are verified in real-time and recorded immutably.

- Lending Platforms – Smart contracts automatically enforce loan conditions, interest calculations, and repayment schedules, reducing manual errors and fraud risks.

- Payment Gateways – Continuous monitoring of payment requests and immutable records prevent unauthorized transfers and phishing attacks.

- Wealth Management & Trading – Blockchain ensures transparency in trades and asset transfers, while Zero Trust prevents unauthorized access to trading accounts or investment data.

These use cases demonstrate how fintech companies can improve operational efficiency and security simultaneously, leveraging cutting-edge technology to protect both their infrastructure and customers.

5. Challenges to Implementation

Despite the advantages, integrating blockchain with Zero Trust comes with challenges:

- Scalability – Blockchain can face throughput limitations, particularly in high-frequency trading or large transaction volumes.

- Complexity of Integration – Combining Zero Trust authentication systems with blockchain infrastructure requires advanced technical expertise and substantial investment.

- Regulatory Uncertainty – Financial regulators are still evaluating how blockchain and Zero Trust affect compliance reporting, data storage, and auditability.

- Cost Considerations – Deploying and maintaining these advanced security frameworks can be expensive for smaller fintech firms without significant capital.

Overcoming these hurdles requires careful planning, phased deployment, and collaboration with regulators to ensure both security and compliance.

6. Future Prospects of Blockchain + Zero Trust in Fintech

The future of fintech security lies in automation, transparency, and proactive threat detection. By 2025–2030, blockchain and Zero Trust architectures are expected to:

- Become Industry Standards – Large banks, neo-banks, and payment platforms will increasingly adopt these frameworks to protect customer data and digital assets.

- Integrate AI & Machine Learning – Predictive AI will complement blockchain and Zero Trust by identifying suspicious transactions or anomalies in real-time.

- Drive Regulatory Compliance – Immutable audit trails and automated enforcement of rules will make regulatory reporting more efficient and accurate.

- Enhance Cross-Border Payments – Blockchain can secure international fund transfers, while Zero Trust ensures authentication and compliance at every step, reducing fraud and settlement times.

India’s fintech sector, with its digital-first mindset, UPI infrastructure, and growing crypto ecosystem, is well-positioned to lead in adopting these advanced security solutions, setting a global example for secure and resilient digital finance.

Conclusion

The combination of blockchain technology and Zero Trust architecture is redefining fintech security. By providing immutable records, smart contract enforcement, continuous monitoring, and strict access controls, this innovative approach addresses both external cyber threats and internal risks.

As fintech adoption accelerates in India and globally, these technologies will be critical for building consumer trust, regulatory compliance, and operational resilience. Companies that implement blockchain + Zero Trust early will not only secure their systems but also gain a competitive edge in a rapidly digitizing financial world.